Your Trading Ideas,

Tested and Running

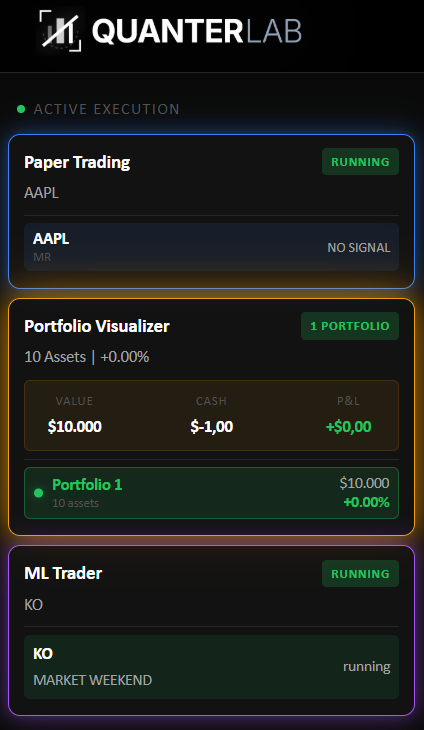

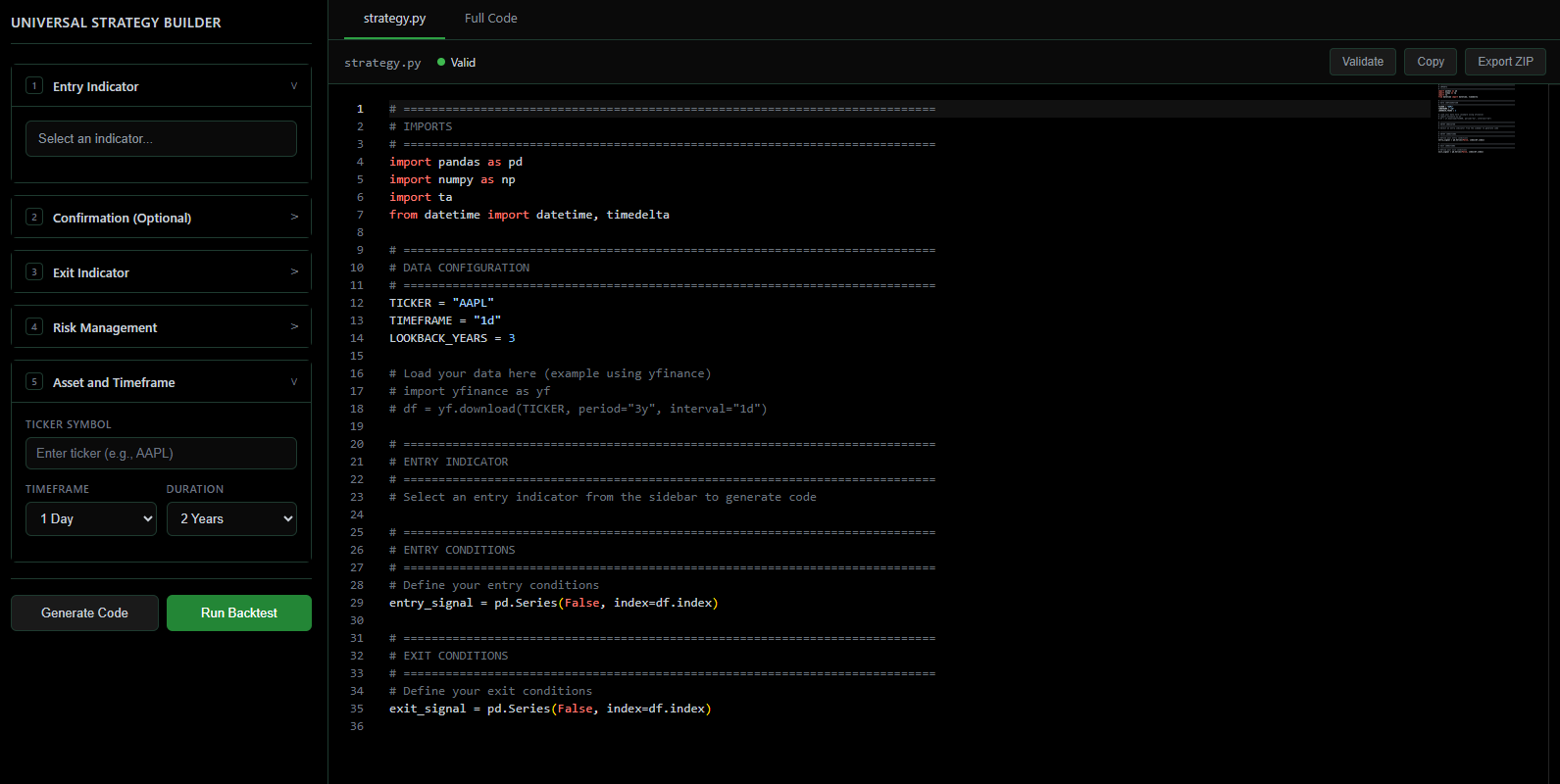

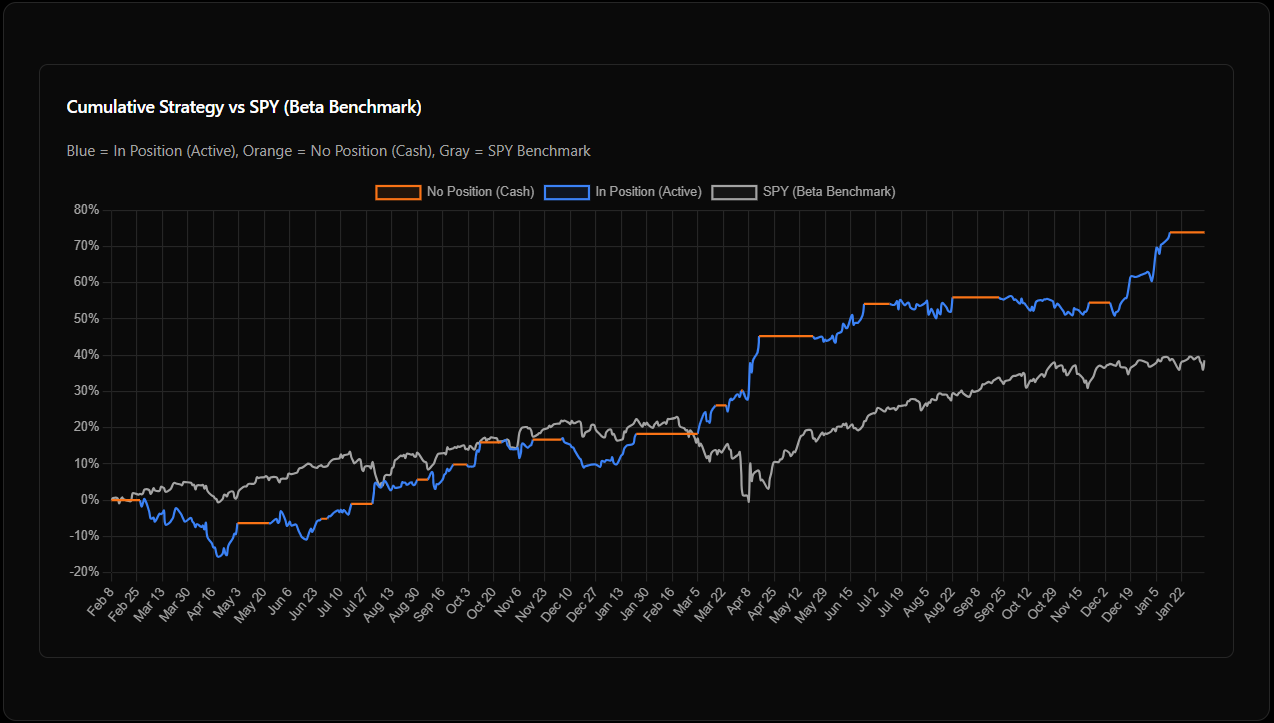

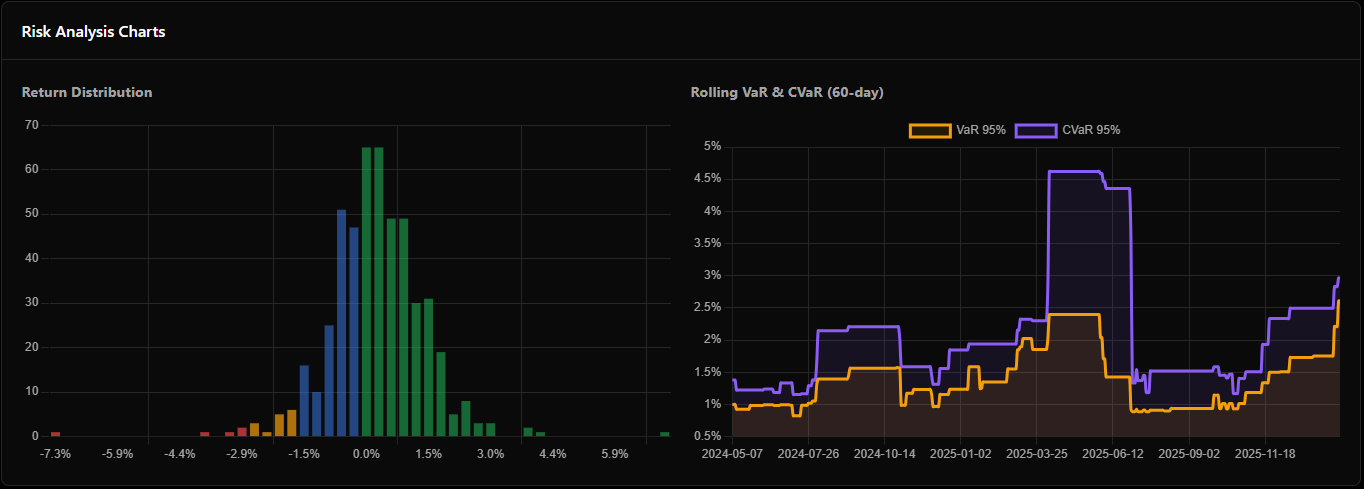

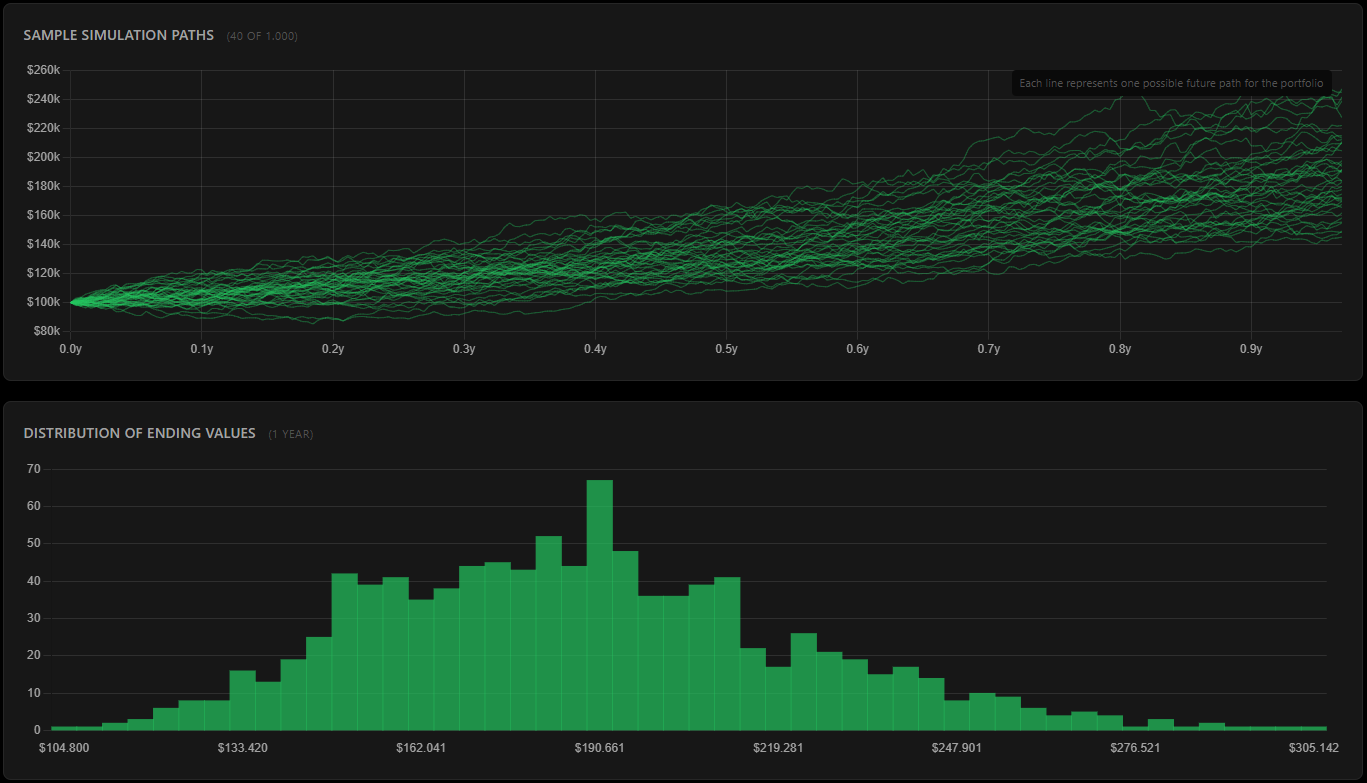

Build indicator strategies, optimize portfolios with MVO & HRP, run Monte Carlo simulations, and analyze risk with VaR/CVaR — no coding required. Backtest, forward-test, and deploy live signals, all in your browser.